Linux and Open Source in Telecommunications

This article examines the impact that Linux and open-source software are having on the telecommunication industry, technology trends moving toward open and standards-based platforms and the .orgs that are active in promoting carrier grade base platforms. Furthermore, this article focuses on the Carrier Grade Linux initiative at OSDL and discusses its contributions to this growing ecosystem.

The telecommunication industry is facing several challenges:

Telecom service providers are looking to reduce their costs using commodity software and commercial off-the-shelf (COTS) hardware building blocks.

Telecom service providers require seamless integration of COTS carrier grade components; the integrated solution must be validated for carrier grade availability.

The growth of packet traffic is putting pressure on communication networks originally designed for “store and forward”; platforms in an all-IP environment that maintain carrier-class characteristics are delivering increasing levels of availability and dependability.

Operators want to decrease time to market and increase the capability for fast delivery of new services by shortening new service development time and unifying platforms.

Of course, operators want to roll out the above capabilities while still making money and increasing profits.

Linux and open-source software provide a compelling avenue to operator success. The open-source operating system has certain characteristics that confer upon it advantages over other operating systems; indeed, Linux has been a disruptive technology with clear impact in telecommunications. Today, not only do many of the server nodes with telecom networks run Linux, but Linux also powers mobile phones and many intermediate nodes “in the middle”.

So, what is a disruptive technology, and how does it impact an industry?

Disruptive technologies first appear saddled with significant deficiencies and are usually targeted at niche segments. Disruptive technologies, however, also provide significant cost benefits. For example, a truly disruptive technology may offer only half the performance of its legacy competitor but can be delivered at one-tenth the cost.

Disruptive technologies are most often taken up by early adopters and then experience a much slower adoption into the mainstream. The adoption of a disruptive technology always starts with non-mission-critical applications (such as utility computing) and moves to mission-critical application as it matures (such as business-critical and enterprise core applications). Linux adoption followed this pattern, starting out hosting Web servers, e-mail and FTP servers and moving now to mission-critical applications, such as telephony. With increasing adoption, a disruptive technology, such as Linux, provides an opportunity (or even forces) companies to re-evaluate and also re-invent their business models and identify real value-added products and services. Companies that do not provide clear value quickly find themselves out of the market.

Linux adoption in telecommunication has not only been increasing, but adoption is also accelerating. Reasons to adopt Linux vary but revolve around common key advantages, such as licensing terms, full access to source code, freedom to choose from multiple providers, lower costs versus legacy and proprietary operating systems, higher system performance, reliability, security, source code quality, innovation rate, peer review, testing resources and the availability of an established ecosystem.

The traditional telecommunication business model is one of high-margin and high-revenue business. In the past, telecom experienced better than 10% year-on-year growth, and almost any project could become successful because demand was so great. Telecommunication companies bought in and sold on proprietary solutions, taking a margin on top of the initial licensing costs. Standards were sufficient only to ensure basic connectivity; after that, essentially proprietary models were built up, with vendor lock-in as the norm.

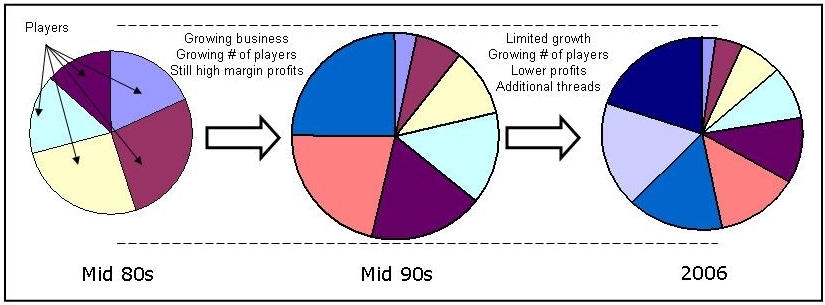

Figure 1. Telephony Business in (R)Evolution: the Business State from the mid-1980s to Today

Figure 1 illustrates the state of the telecom business beginning in the mid-1980s up to the present. In the 1980s, the carrier's business was monopoly-based with very few players in the field, which provided carriers the opportunity to make a lot of money, due to significant margins with voice telephony as a high-priced premium service. In the mid-1990s, new players (carriers/operators) entered the business, increasing the competition. However, voice telephony was still a premium service, and although prices were falling, operators still had significant margins. Today, the business looks very different. It is shrinking with many more players in the space, increased competition and much diminished profits. Voice telephony is a commodity. Furthermore, the industry faces additional threats, such as VoIP and broadband telephony. How can they beat free or close-to-free calling?

In the past (circa 1985), communications and data service networks built on proprietary platforms to meet specific requirements for availability, reliability, performance and service response time. However, communications service providers needed to drive down costs while maintaining carrier-class platforms with high availability, scalability, security, reliability, predictable performance and easy maintenance and upgrade.

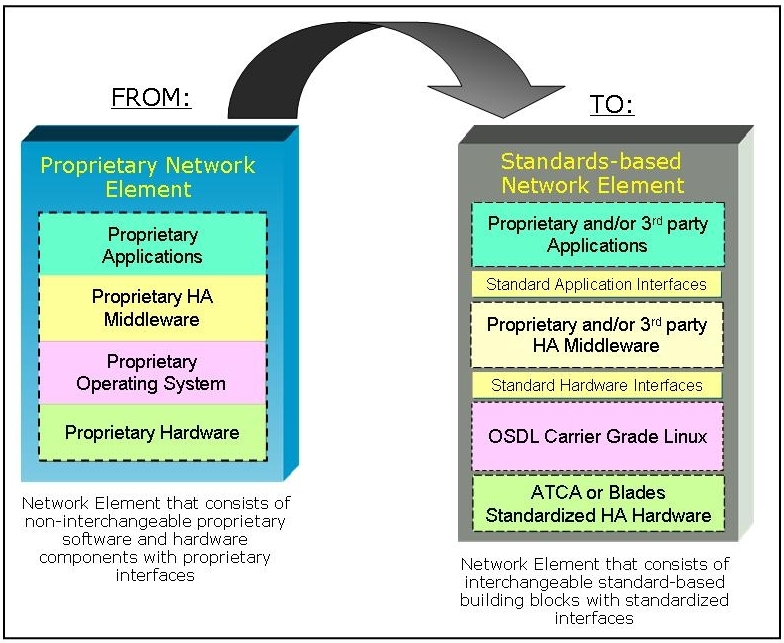

Figure 2. The Technology Trend from Closed Proprietary to Open Standards-Based Platforms

The current technological trend in this space, illustrated in Figure 2, is moving away from expensive proprietary and legacy systems consisting of proprietary technologies and components without a clear separation of the “building blocks” into standards-based systems that consist of interchangeable software and hardware COTS “building blocks” that communicate with each other using standardized interfaces and that are offered by multiple providers.

Traditionally, communications and data service networks were built on proprietary platforms that had to meet very specific requirements in areas such as availability, reliability, performance and service response time. Those proprietary systems were composed of highly purposed hardware, operating system and middleware and often included proprietary technologies and interfaces. Such proprietary approaches to system architecture fostered vendor lock-in, served to limit design flexibility and freedom and produced platforms that are very expensive to maintain and expand.

Today, those same service providers and carriers are challenged to drive down costs while still maintaining carrier-class characteristics for platforms to provide service and mission-critical applications in an all-IP environment. Providers are in a position today where they must move away from specialized proprietary architectures and toward COTS approaches and building practices (Figure 2) for several reasons:

Faster time to market.

Reduced design and operation costs by using COTS hardware and software components.

The growth of packet traffic is placing added pressure on communication networks. Communication platforms reside on all-IP networks and need to maintain carrier grade characteristics in terms of availability, reliability, security and service response time.

The emergence of COTS hardware and software components is driving the need for seamless integration of all components as integrated solutions that must be validated for carrier grade availability and scalability.

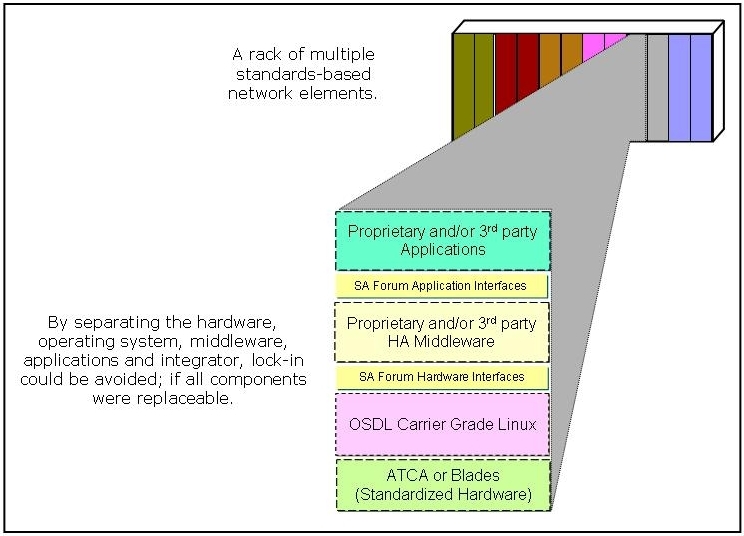

The benefits of a standardized platform (Figure 3) based on COTS hardware and software are many:

Avoiding lock-in: by separating the hardware, operating system, middleware, applications and integration, vendor lock-in can be avoided by making components replaceable and interoperable through standardized interfaces.

The platform achieves economic as well as technical scaling.

All components and ecosystem links, including the integrator, can be changed if they underperform, with minimal impact.

A fully open-source route is possible for next-generation networks and products.

End customers benefit from multiple products running side by side on the platform and from an improved cost base and speed from fewer adopted platforms.

Moving to CGL from a proprietary OS can save telecom equipment manufacturers money because they don't have to develop, maintain or license an in-house proprietary OS. Instead, they can invest in the CGL ecosystem to make Linux good for their own use. In addition, the flexibility of an open-source operating system provides for more customization, increasing each manufacturer's competitive advantage.

Figure 3. A Typical Telecom Rack with Multiple Network Elements

To summarize, the telecommunication industry is transitioning to COTS architectures and practices, embracing Linux and open-source software and re-aligning at multiple levels. Before 1999/2000, the industry experienced incompatible platforms, protocols, high barriers to entry, circuit switches and so on. Today, the telecommunication industry is resurging with COTS, Linux and open-source software, with many new players and many opportunities for new businesses.

Vendor Lock-in

Lock-in is an economic issue, not a technical one. It presents a technology “exit barrier” and takes four steps. First, vendors' offers initially vary—with low cost but proprietary solutions, well-integrated by having just enough standard interfaces and APIs (proprietary is often called “value added” or something similar). Next, vendors offer business-case compelling information, based around the presumed low cost of their solution. The third step is encouraging a strong roll-out of the solution to establish a sufficiently large installed base to start raising costs (license, support and so forth). The fourth and final step is when suppliers raise pricing up to, but not beyond, the point where additional roll-out of their equipment is slightly less expensive than replacing everything with an alternative vendor's. The exit barrier has been raised, and you are now locked in.

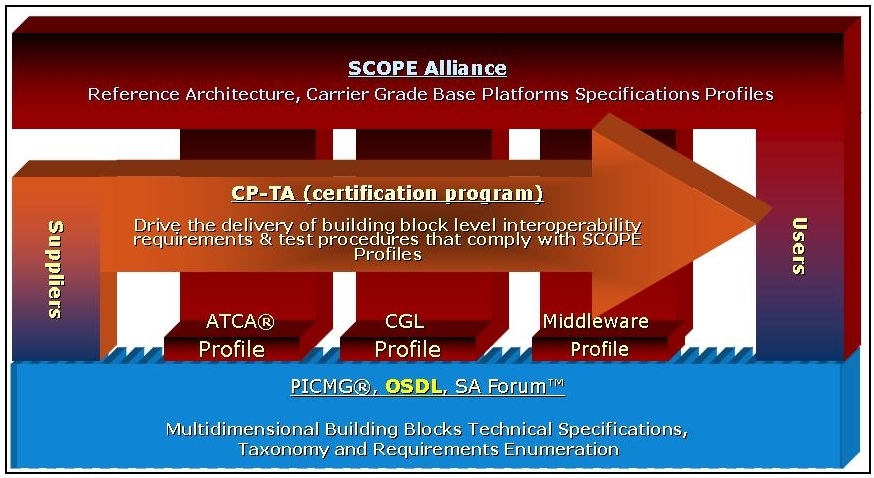

There are five major .orgs (Figure 4) active in the space of accelerating the adoption of carrier grade platforms that are based on COTS hardware and software. These organizations are CP-TA, OSDL, PICMG, SA Forum and the SCOPE Alliance. In the following sections, we present each of these organizations, discuss their goals and highlight their contributions.

Figure 4. The .org Players: PICMG, OSDL, SA Forum, CP-TA and the SCOPE Alliance (courtesy CP-TA)

The Communications Platforms Trade Association (CP-TA) is a group of communications platform and building block providers dedicated to accelerating the adoption of SIG-governed, open specification-based communications platforms through interoperability testing and certification. With industry collaboration, CP-TA plans to drive a mainstream market for open industry standards-based communications platforms.

The Service Availability Forum (SA Forum) is a consortium of communications and computing companies working together to develop and publish high-availability and management software interface specifications.

The OSDL Carrier Grade Linux (CGL) initiative is an industry forum that supports and accelerates the development of Linux functionality for telecommunication applications. The goal of CGL is to make Linux better for the telecommunication industry. A Linux kernel with carrier grade characteristics is an essential component in open, standards-based communication platforms and architectures. OSDL specifically focuses its work on the Linux operating system and collaborates with other industry organizations to drive adoption of open standards and open-source software. It works closely with each group to ensure that efforts are complementary and deliver value to the market.

The SCOPE Alliance is an industry alliance committed to accelerating the deployment of carrier grade base platforms for service provider applications. Its mission is to help, enable and promote the availability of open carrier grade platforms based on (COTS) hardware and software and Free and Open-Source Software (FOSS) building blocks and to promote interoperability to better serve service providers and consumers.

The PCI Industrial Computer Manufacturers Group (PICMG) is a consortium of more than 450 companies who collaboratively develop open specifications for high-performance telecommunications and industrial computing applications. The consortium has resulted in a series of specifications that include CompactPCI, AdvancedTCA, AdvancedMC, CompactPCI Express, COM Express and SHB Express. The goal of PICMG is to offer equipment vendors common specifications, thereby increasing availability and reducing costs and time to market.

The OSDL Carrier Grade Linux working group was established in January 2002. Its goal is to identify requirements for enhancing the Linux operating system to achieve an open-source platform that is highly available, reliable, secure and scalable, and suitable for carrier grade systems. The CGL working group has the vision that next-generation and multimedia communication services can be delivered using Linux-based platforms. To realize this vision, the work group developed a strategy to define the requirements and architecture for the Carrier Grade Linux platform and promote development of a stable platform for deployment of commercial components and services.

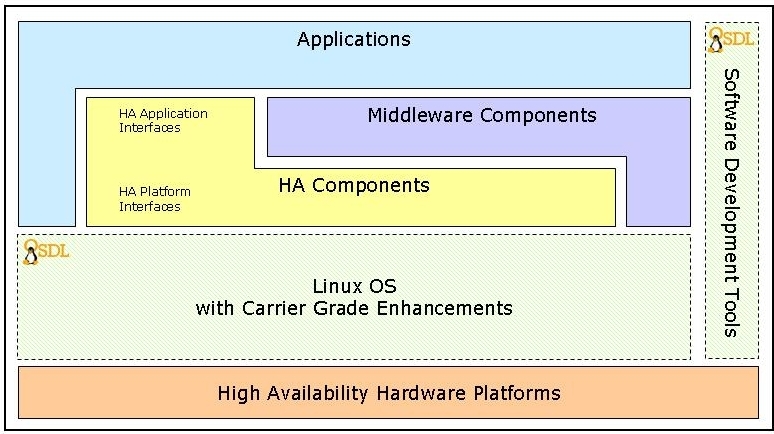

Figure 5. Scope of the Carrier Grade Linux Working Group

The CGL working group focuses on two areas: carrier grade enhancements to the operating system that are related to various requirements, such as availability and scalability, and software development tools. Today, more than two-dozen OSDL member companies from all over the globe are actively involved with the CGL initiative. Member companies cover the whole ecosystem: carriers, network equipment providers (NEPs), telecom equipment manufacturers (TEMs), platform providers, independent software vendors (ISVs), middleware providers and Linux distributors.

The CGL working group also identifies existing open-source projects that map to the CGL requirements. The result is the CGL Development Guideline Web site (see the on-line Resources). This is an effort from the CGL initiative to survey open source for projects that can potentially provide implementations for the requirements defined in the CGL Requirements Documents. This site is maintained and updated frequently.

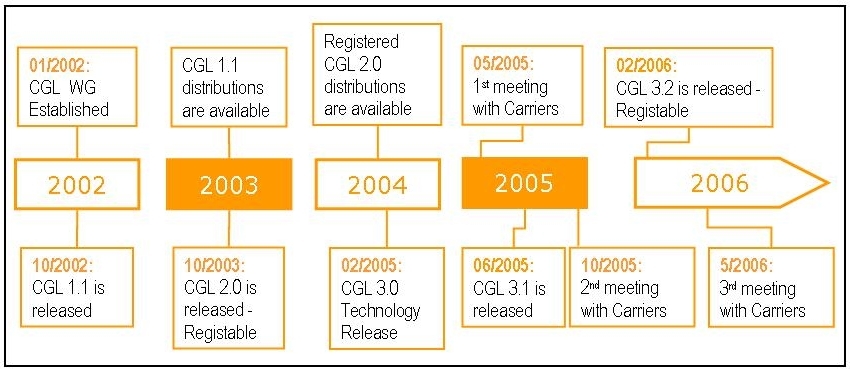

Figure 6. Overview of the CGL Initiative from Its Inception in 2002 to June 2006

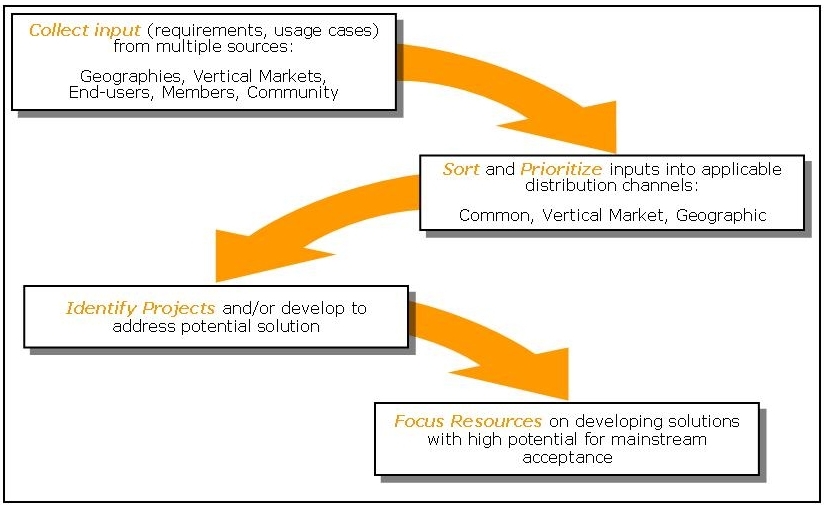

The CGL working group collects requirements from multiple industry sources and develops use cases for the various proposed capabilities and functionalities. The working group then sorts and prioritizes the input from the industry, member companies and end users to identify open-source projects that are working on these areas. If no open-source project exists, the working group starts new open-source projects to develop these capabilities and focuses its resources to develop solutions with high potential for mainstream acceptance. In many instances, member companies have (re)released previously proprietary technologies as open source to accelerate the availability of these capabilities in Linux.

Figure 7. The CGL Initiative Work Process

The CGL initiative released the original CGL Requirement Definition Document in 2002 (v1.1) and has issued two revisions (v2.0 and v3.2), and it also has established a registration process for Linux vendors to register compliance of their Linux distributions.

CGL and the COTS Ecosystem

CGL is an important part of the telecommunications move to using COTS components for building equipment. Carriers and service providers are in a position today where they must move away from specialized proprietary architectures toward COTS approaches and building practices for several reasons, such as reducing design and operation costs and gaining the ability to deliver new services faster based on common standardized platforms. In addition, the increased power and reliability of such building blocks, along with the development of specifications that guide their implementation, are allowing more flexibility for network deployment with improved price performance. CGL is a core building block, providing a Linux kernel that offers the needed reliability, availability and performance for platforms running in mission-critical environments and providing communication services.

The CGL working group established a registration process for Linux distributions to disclose information on how they meet the CGL requirements. The process is a public disclosure of all CGL requirements as mandated by each CGL release version and describes how the Linux vendor met the CGL requirements. The outcome of the registration process allows CGL-registered platform suppliers to market their Linux distributions and systems to NEPs and TEMs and carriers with the CGL registration mark to demonstrate the platform's suitability for carrier grade applications.

In June 2006, Debian passed the CGL 2.0 registration process, becoming the seventh distribution that meets the CGL 2.0 requirements. The other six are Asianux, FSMLabs, MontaVista, Novell, TimeSys and Wind River. The Debian announcement is of great importance. Debian is one of the leading distributions of the Linux operating system. Its registration adds more than 1,000 developers and tens of thousands of end users to the CGL community. Debian registration gives telecommunications providers a fully open platform that comes with the support of one of the strongest Linux communities and represents an ideal balance between “roll-your-own” CGL solutions and available commercial options. Telecommunications equipment providers looking for a fully open option now have one.

CGL Initiative Achievements:

Increasing the number of OSDL member companies involved with CGL; the latest members include Siemens and Motorola.

Three major releases of the CGL Requirement Definition Documents: CGL V1.1 in October 2003, CGL 2.0 in October 2003 and CGL 3.2 in February 2006.

Seven distributions and Linux vendors registered for CGL 2.0: TimeSys, Novell/SUSE, MontaVista, FSMLabs, WindRiver, Asianux and Debian. Linux vendors are now in the process of registering for compliance with CGL 3.2.

More than 25 platform providers are integrating CGL as part of their offering.

Service providers and carriers are deploying CGL-based platforms.

In the February 2006 LinuxWorld magazine editorial, “The Holy Grail of Networking”, Stuart Cohen, CEO of OSDL, discussed the end-to-end infrastructure with a single operating system (Linux) and the role OSDL is playing to enable this single OS infrastructure from the server to the handset. At OSDL, the CGL and MLI initiatives are driving forward an “end-to-end” Linux deployment, succeeding in its mission to accelerate the development and adoption of Linux from the enterprise to mobile computing in a vertical industry that has been historically dominated by proprietary technologies. What's next for Linux? Only time will tell.

To learn more about how OSDL initiatives are helping accelerate the development and adoption of Linux, visit the OSDL Web site (see Resources).

The author would like to thank Bill Weinberg, OSDL's Senior Technology Analyst, for his valuable reviews and contributions.

Resources for this article: /article/9267.

Ibrahim Haddad manages the Carrier Grade Linux and the Mobile Linux Initiatives at OSDL, promotes the development and adoption of Linux in the Communication industry, and leads the Carriers/NEPs Forum he established at OSDL in early 2005. Prior to joining OSDL, Ibrahim was a Senior Researcher at the “Research and Innovation” Department of Ericsson Corporate Unit of Research in Montréal, Canada, where he was involved with the server system architecture for 3G wireless IP networks and contributed to Ericsson's open platform efforts. Ibrahim is co-author of two books on Red Hat Linux and Fedora, and a Contributing Editor of three leading Linux publications. Ibrahim received his PhD in Computer Science from Concordia University in Montréal, Canada.